Last Updated: 03/19/2026

If you have a felony on your record and you want to start a business, getting funding is possible, but you need to be realistic about which options are actually worth your time.

There are not many true business loans made specifically for felons. What exists instead are standard small business funding options that may still be available to you depending on your credit, business plan, time since conviction, current legal status, and the lender’s own rules. The good news is that SBA (Small Business Administration) rules became more open in 2024, removing many older criminal history barriers that used to block qualified applicants.

The most important thing to know is this: a felony does not automatically disqualify you from every small business loan. But some situations still create major problems. Under current SBA rules, businesses are ineligible if an associate is currently incarcerated, serving a sentence of imprisonment, or under indictment for a felony or a crime involving financial misconduct or a false statement. SBA also said people who previously defrauded the government remain ineligible.

For many people with records, the best path is not chasing a giant bank loan on day one. It is usually smarter to start with a small amount of capital, build basic business credit and revenue, and then move up to larger funding later.

Quick Answer

Yes, felons can get small business loans.

Your best odds are usually with:

- SBA Microloans

- CDFI and community lenders

- Online lenders for established revenue

- Business credit cards used carefully

- Free business training and planning help before you apply

If your credit is weak, your business is brand new, and you do not yet have a real plan or revenue, you will probably struggle with traditional lenders. In that case, your first goal should be getting lender ready, not just filling out more applications.

Best Small Business Loan Options For Felons

1. SBA Microloans (Small Business Administration)

For most readers, this is the strongest place to start.

The SBA Microloan program offers loans of up to $50,000, and the average microloan is about $13,000. These loans are made through nonprofit community lenders, not directly by SBA, and those lenders often provide coaching and technical assistance along with the loan. That matters because many people with felony records need guidance as much as funding.

Why this option stands out:

- The loan size is more realistic for a new business.

- Community lenders are often more flexible than banks.

- Many microloan programs care a lot about your plan, your preparation, and your ability to repay.

- You may also get business training at the same time.

This is especially useful for service businesses, home based businesses, lawn care, cleaning, mobile detailing, pressure washing, trucking support, handyman work, food service startups, and other businesses that do not need huge capital up front.

2. SBA 7(a) Loans

SBA 7(a) loans are the big mainstream small business loan program. The maximum loan amount is $5 million. These loans can be used for a wide range of business purposes, but they are harder to get than microloans. Lenders still look closely at credit history, repayment ability, time in business, cash flow, and overall risk.

A 7(a) loan is usually a better fit if:

- You already have a real business

- You can show revenue

- Your credit has recovered

- You have clean financial records

- You need growth capital, not just startup money

If you are just getting started, this is usually not the first loan I would chase.

3. SBA 504 Loans

SBA 504 loans are mainly for major fixed assets, such as buying real estate, land, buildings, or large equipment. The maximum loan amount is $5.5 million. This is not the right fit for most people looking for startup cash or a small first business.

If your goal is to buy a building, purchase large machinery, or finance a serious long term expansion, this can be a strong program later on. But for most people searching this keyword, 504 is too advanced for the first move.

4. CDFI and Community Lenders

CDFIs can be one of the most practical paths for people who feel shut out by traditional banks.

These mission focused lenders often work in underserved communities and may be more willing to look at the whole picture instead of reducing you to one felony background issue. They are not guaranteed approvals, but they are often a smarter option than going straight to a major bank with a thin file. You can search for organizations in your state through CDFI databases and locator tools.

This route makes sense if you have:

- A small business plan

- Modest capital needs

- Weak or rebuilding credit

- Some income or realistic repayment ability

- A need for coaching, not just money

5. Online Business Lenders

Online lenders may be faster and easier to access than traditional banks, especially if your business already has some revenue. But the tradeoff is usually higher cost.

This route can help if you have sales coming in and need working capital fast. It is usually a weaker fit for brand new businesses with no revenue, and it can become expensive if you borrow before your business is stable. Competing guides ranking now also include online lenders as a practical option when SBA or bank financing is not realistic.

6. Business Credit Cards

A business credit card is not the same thing as a loan, but for some felons it is one of the easiest ways to access short term capital.

This can work well if you are disciplined, need a small amount of money, and can pay the balance down quickly. It can also help you separate business spending from personal spending. But if you use it to fund a weak business idea or carry a balance too long, it can make your situation worse.

Who Has The Best Chance Of Approval?

You are more likely to get approved if most of these are true:

- Your felony conviction is older

- You are not currently incarcerated

- You are not under indictment

- Your record does not involve financial misconduct or false statements that raise lender concerns

- Your personal credit is at least improving

- You have stable income or business revenue

- You have a simple, realistic business plan

- You are asking for a modest amount, not a huge amount

- You can clearly explain how the money will be used

- You have already done some of the work yourself

Lenders want to see risk shrinking, not excuses growing.

Who Will Have A Harder Time?

You may struggle more if:

- Your credit is very poor

- You have unpaid judgments, collections, or tax problems

- You want a large startup loan with no revenue

- Your business idea is vague

- Your paperwork is sloppy

- Your offense involved fraud, theft, or financial deception and the lender sees a direct risk connection

- You are applying before you have shown any stability

That does not mean give up. It means you may need to fix the file first.

What To Do Before You Apply

1. Build a real business plan

You do not need a huge fancy document, but you do need a clear plan that answers:

- What are you selling?

- Who will buy it?

- Why will they choose you?

- How much do you need?

- Exactly what will the money pay for?

- How will you repay it?

Good information on how to write a business plan.

2. Start smaller than you want

One of the biggest mistakes people make is trying to borrow too much too early. A lender is much more likely to consider a smaller request tied to a clear use of funds than a vague request for a big amount.

3. Get free business help first

Before you apply anywhere, use a local Small Business Development Center. America’s SBDC says local centers offer no cost business consulting and low cost training. This is one of the best free steps you can take before applying for any loan.

4. Improve your credit before chasing a bigger loan

If your credit is weak, focus on paying on time, lowering utilization, checking for errors, and avoiding desperate applications that create multiple hard pulls.

5. Separate your business from your personal life

Open a business bank account when appropriate, track your income and expenses, and keep your records clean. A messy file makes a lender nervous fast.

Best Free Resources For Felons Starting A Business

Small Business Development Centers

SBDCs help with business plans, startup questions, growth strategy, and training. Their site says you can find your nearest center by ZIP code or state, and that they offer no cost consulting.

Inmates to Entrepreneurs

Inmates to Entrepreneurs offers a free, self paced online course that teaches how to start, run, and grow a business with a felony record. Their course covers business ideas, marketing, hiring, financing, money management, and launch planning.

Defy Ventures

Defy Ventures runs programs for people with criminal histories focused on skills, connections, confidence, employment readiness, and entrepreneurship support.

CDFI Locator Tools

CDFI resources can help you find mission driven lenders and organizations in your state that may be more accessible than a major bank.

The Honest Truth About Grants

A lot of people search for loans when what they really want is free money.

Real small business grants do exist, but they are competitive and there are not many grants created specifically for felons. Even strong pages ranking right now mix grants, loans, and entrepreneurship support because most readers need a combination of all three, not just one magic funding source.

That means you should not sit around waiting for a perfect grant. In many cases, the better move is:

- Start small

- Use free training

- Build proof of concept

- Apply for a small realistic loan later

Scam Warning

Be careful with anyone promising:

- Guaranteed approval

- Instant government money

- Secret felony grants

- Large startup funding with no paperwork

- Approval only after a large upfront fee

Good lenders ask hard questions. Scammers avoid them.

Our Recommendation

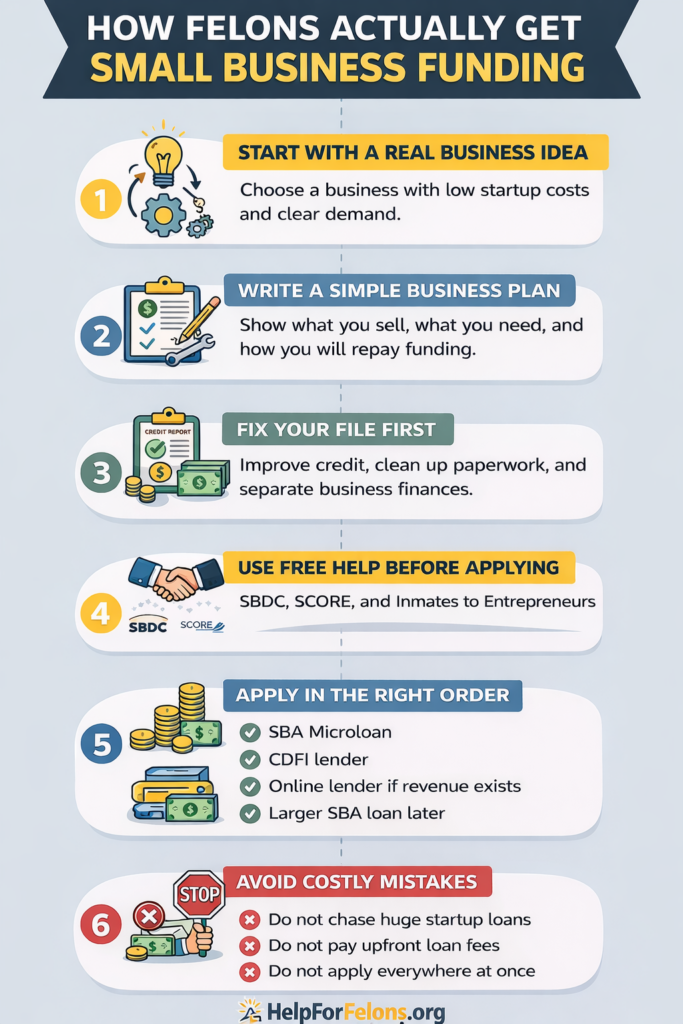

If you have a felony and want to start a business, I would usually follow this order:

- Get free help from an SBDC

- Tighten your business plan

- Fix your credit if needed

- Look at SBA Microloans and local CDFI lenders first

- Use online lenders only when you understand the cost

- Move up to larger funding only after you show real traction

That path is slower, but it is much more realistic.

FAQ Small Business Loans For Felons

Sometimes, yes. SBA rules are more open than they used to be, but businesses are still ineligible if an associate is currently incarcerated, serving a sentence of imprisonment, or under indictment for a felony or a crime involving financial misconduct or a false statement.

Not always. But many lenders still look at overall risk, including credit, cash flow, time in business, paperwork quality, and whether your background raises concerns tied to the type of loan.

There are some resources and occasional opportunities, but not many true grants built specifically for this group. Most people will need to combine free support, low cost startup methods, and practical financing options. We do have a Grants For Felons Page.

Disclaimer

This page is for general informational purposes only and is not legal, financial, or lending advice. Loan approval depends on the lender, your credit, your business, your legal status, and current program rules. Always verify eligibility and loan terms directly with the lender or official program source before applying.